What shaped the past week?

Global: Global markets traded in a bearish manner this week, as major markets across the globe closed in the red w/w. Starting in Asia, sentiment in the region remains weighed down by movement restrictions in China, as the country continues to battle the COVID pandemic.

The Royal Bank of Australia highlighted that it is appropriate to start lifting certain monetary support measures, while Tokyo's inflation was reported to be 2.5%, year-on-year, in April. For the week the Shanghai Composite eased 1.49% while the Nikkei-225 recorded modest gains, rising 0.58% w/w. Moving to the European region, sentiment was sell-side driven, with all major markets in the space closing in the red. Notably, the German Dax eased 3.02% w/w, with the French CAC and London based FTSE-100 dipping 4.45% and 0.98% respectively at time of writing. The U.S. Fed's latest announcement on the 0.5% interest rate hike seemingly rocked stock markets across the globe. Finally, moving to the United States, sentiment was largely bearish as well; tech stocks continue to see aggressive sell-side action in the space as the NASDAQ eased 1.15% w/w, with the SP 500 and Dow Jones down 0.28% and 0.52% w/w. Earlier in the week, the United States Federal Reserve raised rates by 50bps to take the monetary policy rate to 1.00% and this weighed on investor sentiment in the equities space.

The Royal Bank of Australia highlighted that it is appropriate to start lifting certain monetary support measures, while Tokyo's inflation was reported to be 2.5%, year-on-year, in April. For the week the Shanghai Composite eased 1.49% while the Nikkei-225 recorded modest gains, rising 0.58% w/w. Moving to the European region, sentiment was sell-side driven, with all major markets in the space closing in the red. Notably, the German Dax eased 3.02% w/w, with the French CAC and London based FTSE-100 dipping 4.45% and 0.98% respectively at time of writing. The U.S. Fed's latest announcement on the 0.5% interest rate hike seemingly rocked stock markets across the globe. Finally, moving to the United States, sentiment was largely bearish as well; tech stocks continue to see aggressive sell-side action in the space as the NASDAQ eased 1.15% w/w, with the SP 500 and Dow Jones down 0.28% and 0.52% w/w. Earlier in the week, the United States Federal Reserve raised rates by 50bps to take the monetary policy rate to 1.00% and this weighed on investor sentiment in the equities space.

Domestic Economy: Recently, the Federal Government of Nigeria ordered the reopening of four additional land borders - Idiroko (Ogun), Jibiya (Kastina), Kamba (Kebbi), and Ikom (Cross Rivers) borders. This is happening two years after the reopening of the Seme (Lagos), Maigatari (Jigawa), Illela (Sokoto), and Mfum (Cross River) borders ahead of the take-off of the Africa Continental Free Trade Area (AfCFTA). While the borders were closed to prevent the smuggling of weapons and support the local cultivation of food, the prices of food items have risen nonetheless as supply fails to keep up with demand. In the near term, we expect the reopening of the borders to support volatile food supply from food-producing states, boost intra-African trade and culminate to lower inflation outcomes.

Domestic Economy: Recently, the Federal Government of Nigeria ordered the reopening of four additional land borders - Idiroko (Ogun), Jibiya (Kastina), Kamba (Kebbi), and Ikom (Cross Rivers) borders. This is happening two years after the reopening of the Seme (Lagos), Maigatari (Jigawa), Illela (Sokoto), and Mfum (Cross River) borders ahead of the take-off of the Africa Continental Free Trade Area (AfCFTA). While the borders were closed to prevent the smuggling of weapons and support the local cultivation of food, the prices of food items have risen nonetheless as supply fails to keep up with demand. In the near term, we expect the reopening of the borders to support volatile food supply from food-producing states, boost intra-African trade and culminate to lower inflation outcomes.

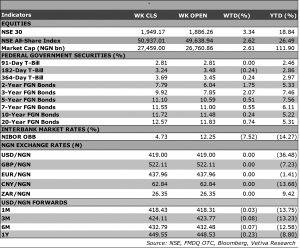

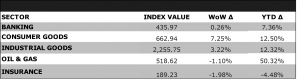

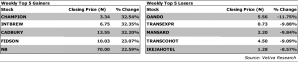

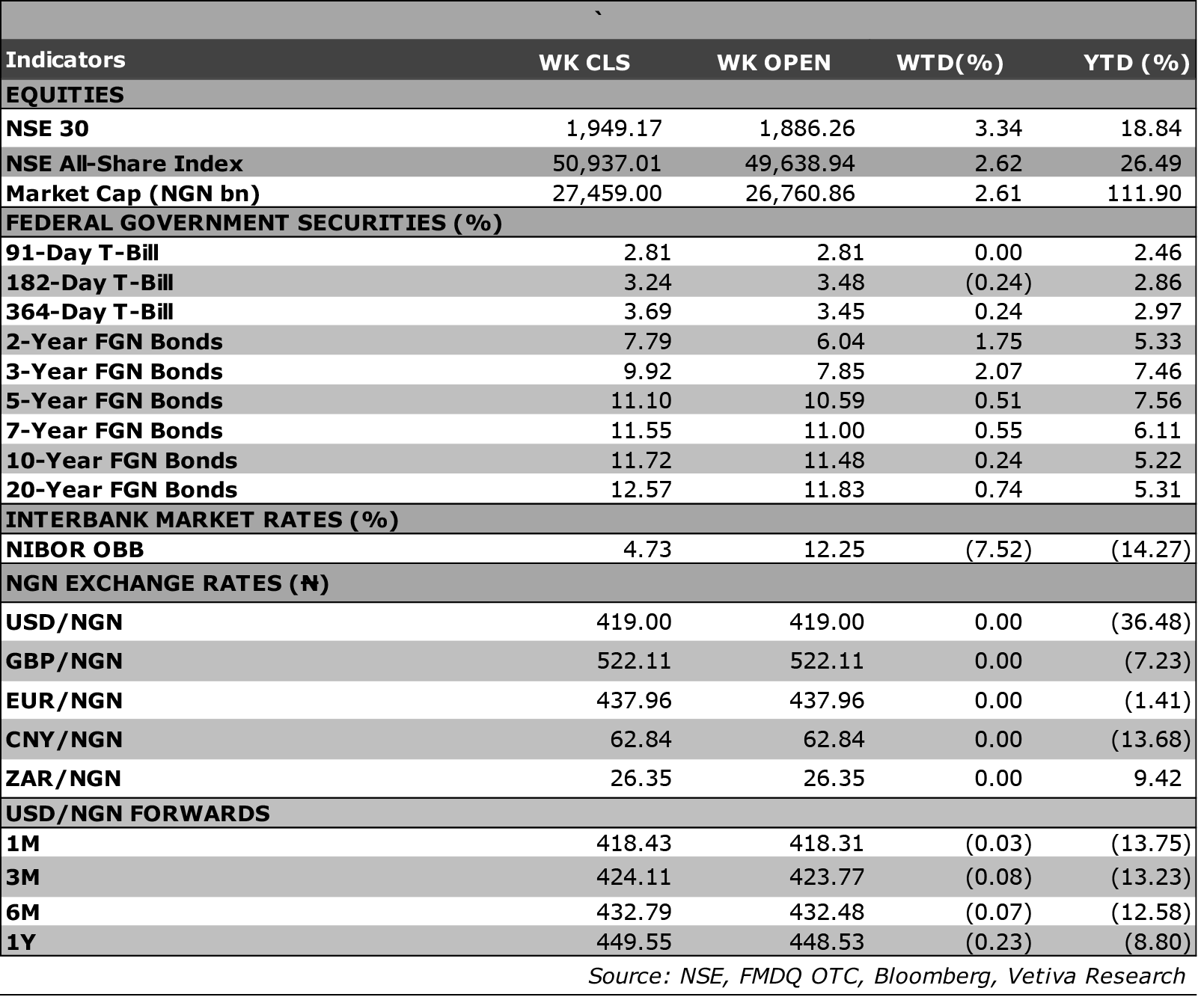

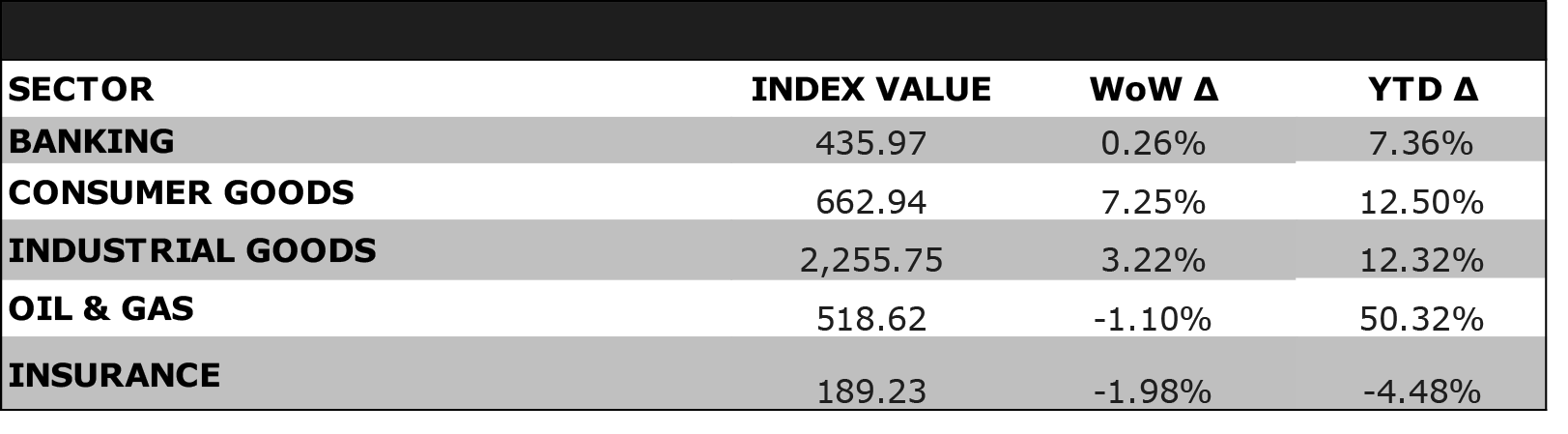

Equities: Nigeria equities extended last week’s gains into this week, as the NGX rose 2.62% w/w, to settle at 50,937pts; taking its YTD performance to +19.24%, which is the highest in the west African region. The Consumer Goods Space was the best performer this week, rising 7.25%, fueled by buy-side action in the breweries space, with INTEBREW and NB rising 32.35% and 22.59% w/w to settle at 6.75/share and 70/share respectively. Likewise, broad based gains across the NGX saw the Banking sector climb 0.26%. Moving to the Industrial Goods space, persistent interest in WAPCO (+1.85% w/w) amongst other players in the space, saw the sector rise 3.22% w/w. Finally, in the Oil and Gas space, the sector eased 1.10% following sessions of strong gains recorded in the sector.

Fixed Income: The fixed income market traded largely bearish, with yields trending upwards in the bonds and NTB spaces, while the OMO segment majorly saw bullish activities. For the week, the yield on benchmark bonds rose 9bps on average, driven by sell-side action at the short-end of the market. Similarly, the NTB saw selloffs at the midpoint of the curve consequently average yield increased 12bps. Finally, in the OMO space yields declined 3bps on average, driven by buy-side activity at the short end of the market.

Equities: Nigeria equities extended last week’s gains into this week, as the NGX rose 2.62% w/w, to settle at 50,937pts; taking its YTD performance to +19.24%, which is the highest in the west African region. The Consumer Goods Space was the best performer this week, rising 7.25%, fueled by buy-side action in the breweries space, with INTEBREW and NB rising 32.35% and 22.59% w/w to settle at 6.75/share and 70/share respectively. Likewise, broad based gains across the NGX saw the Banking sector climb 0.26%. Moving to the Industrial Goods space, persistent interest in WAPCO (+1.85% w/w) amongst other players in the space, saw the sector rise 3.22% w/w. Finally, in the Oil and Gas space, the sector eased 1.10% following sessions of strong gains recorded in the sector.

Fixed Income: The fixed income market traded largely bearish, with yields trending upwards in the bonds and NTB spaces, while the OMO segment majorly saw bullish activities. For the week, the yield on benchmark bonds rose 9bps on average, driven by sell-side action at the short-end of the market. Similarly, the NTB saw selloffs at the midpoint of the curve consequently average yield increased 12bps. Finally, in the OMO space yields declined 3bps on average, driven by buy-side activity at the short end of the market.

|

The Royal Bank of Australia highlighted that it is appropriate to start lifting certain monetary support measures, while Tokyo's inflation was reported to be 2.5%, year-on-year, in April. For the week the Shanghai Composite eased 1.49% while the Nikkei-225 recorded modest gains, rising 0.58% w/w. Moving to the European region, sentiment was sell-side driven, with all major markets in the space closing in the red. Notably, the German Dax eased 3.02% w/w, with the French CAC and London based FTSE-100 dipping 4.45% and 0.98% respectively at time of writing. The U.S. Fed's latest announcement on the 0.5% interest rate hike seemingly rocked stock markets across the globe. Finally, moving to the United States, sentiment was largely bearish as well; tech stocks continue to see aggressive sell-side action in the space as the NASDAQ eased 1.15% w/w, with the SP 500 and Dow Jones down 0.28% and 0.52% w/w. Earlier in the week, the United States Federal Reserve raised rates by 50bps to take the monetary policy rate to 1.00% and this weighed on investor sentiment in the equities space.

The Royal Bank of Australia highlighted that it is appropriate to start lifting certain monetary support measures, while Tokyo's inflation was reported to be 2.5%, year-on-year, in April. For the week the Shanghai Composite eased 1.49% while the Nikkei-225 recorded modest gains, rising 0.58% w/w. Moving to the European region, sentiment was sell-side driven, with all major markets in the space closing in the red. Notably, the German Dax eased 3.02% w/w, with the French CAC and London based FTSE-100 dipping 4.45% and 0.98% respectively at time of writing. The U.S. Fed's latest announcement on the 0.5% interest rate hike seemingly rocked stock markets across the globe. Finally, moving to the United States, sentiment was largely bearish as well; tech stocks continue to see aggressive sell-side action in the space as the NASDAQ eased 1.15% w/w, with the SP 500 and Dow Jones down 0.28% and 0.52% w/w. Earlier in the week, the United States Federal Reserve raised rates by 50bps to take the monetary policy rate to 1.00% and this weighed on investor sentiment in the equities space.

Domestic Economy: Recently, the Federal Government of Nigeria ordered the reopening of four additional land borders - Idiroko (Ogun), Jibiya (Kastina), Kamba (Kebbi), and Ikom (Cross Rivers) borders. This is happening two years after the reopening of the Seme (Lagos), Maigatari (Jigawa), Illela (Sokoto), and Mfum (Cross River) borders ahead of the take-off of the Africa Continental Free Trade Area (AfCFTA). While the borders were closed to prevent the smuggling of weapons and support the local cultivation of food, the prices of food items have risen nonetheless as supply fails to keep up with demand. In the near term, we expect the reopening of the borders to support volatile food supply from food-producing states, boost intra-African trade and culminate to lower inflation outcomes.

Domestic Economy: Recently, the Federal Government of Nigeria ordered the reopening of four additional land borders - Idiroko (Ogun), Jibiya (Kastina), Kamba (Kebbi), and Ikom (Cross Rivers) borders. This is happening two years after the reopening of the Seme (Lagos), Maigatari (Jigawa), Illela (Sokoto), and Mfum (Cross River) borders ahead of the take-off of the Africa Continental Free Trade Area (AfCFTA). While the borders were closed to prevent the smuggling of weapons and support the local cultivation of food, the prices of food items have risen nonetheless as supply fails to keep up with demand. In the near term, we expect the reopening of the borders to support volatile food supply from food-producing states, boost intra-African trade and culminate to lower inflation outcomes.

Equities: Nigeria equities extended last week’s gains into this week, as the NGX rose 2.62% w/w, to settle at 50,937pts; taking its YTD performance to +19.24%, which is the highest in the west African region. The Consumer Goods Space was the best performer this week, rising 7.25%, fueled by buy-side action in the breweries space, with INTEBREW and NB rising 32.35% and 22.59% w/w to settle at 6.75/share and 70/share respectively. Likewise, broad based gains across the NGX saw the Banking sector climb 0.26%. Moving to the Industrial Goods space, persistent interest in WAPCO (+1.85% w/w) amongst other players in the space, saw the sector rise 3.22% w/w. Finally, in the Oil and Gas space, the sector eased 1.10% following sessions of strong gains recorded in the sector.

Fixed Income: The fixed income market traded largely bearish, with yields trending upwards in the bonds and NTB spaces, while the OMO segment majorly saw bullish activities. For the week, the yield on benchmark bonds rose 9bps on average, driven by sell-side action at the short-end of the market. Similarly, the NTB saw selloffs at the midpoint of the curve consequently average yield increased 12bps. Finally, in the OMO space yields declined 3bps on average, driven by buy-side activity at the short end of the market.

Equities: Nigeria equities extended last week’s gains into this week, as the NGX rose 2.62% w/w, to settle at 50,937pts; taking its YTD performance to +19.24%, which is the highest in the west African region. The Consumer Goods Space was the best performer this week, rising 7.25%, fueled by buy-side action in the breweries space, with INTEBREW and NB rising 32.35% and 22.59% w/w to settle at 6.75/share and 70/share respectively. Likewise, broad based gains across the NGX saw the Banking sector climb 0.26%. Moving to the Industrial Goods space, persistent interest in WAPCO (+1.85% w/w) amongst other players in the space, saw the sector rise 3.22% w/w. Finally, in the Oil and Gas space, the sector eased 1.10% following sessions of strong gains recorded in the sector.

Fixed Income: The fixed income market traded largely bearish, with yields trending upwards in the bonds and NTB spaces, while the OMO segment majorly saw bullish activities. For the week, the yield on benchmark bonds rose 9bps on average, driven by sell-side action at the short-end of the market. Similarly, the NTB saw selloffs at the midpoint of the curve consequently average yield increased 12bps. Finally, in the OMO space yields declined 3bps on average, driven by buy-side activity at the short end of the market.