What shaped the past week?

Global: Global markets traded in a bearish manner this week, as investors remain unnerved over the possibilities of a global recession. Investor focus shifted to the latest policy meetings from key central banks, where we saw another round of rate hikes from monetary officials. Starting in the Asian-Pacific region, where the focus was on the latest batch of economic data out of the region, China saw retail sales fall 5.9% y/y, while industrial production came in at 2% y/y, however both data prints were below market expectations; for the week, the Shanghai Composite lost 1.22% w/w, with the Nikkei-225 and ASX falling 1.34% and 0.89% w/w respectively.

Moving to the European region, the latest rate hike from the European Central Bank dragged investor confidence, as they remain concerned about the impact of a restrictive monetary environment on the economy. The ECB raised its cash rate by 50bps to 2.00%, with ECB President Christine Lagarde telling market participants not to expect an early end to the current tightening stance of the ECB. The Bank of England also raised its cash rate as well by 50bps, with BoE governor Andrew Bailey stating that a constrained labor market, rising wages and prices warranted more “forceful” restrictive actions from the BoE. For the week, the German Dax and London FTSE sank 3.38% and 1.96% w/w respectively. Moving to the European region, the latest rate hike from the European Central Bank dragged investor confidence, as they remain concerned about the impact of a restrictive monetary environment on the economy. The ECB raised its cash rate by 50bps to 2.00%, with ECB President Christine Lagarde telling market participants not to expect an early end to the current tightening stance of the ECB. The Bank of England also raised its cash rate as well by 50bps, with BoE governor Andrew Bailey stating that a constrained labor market, rising wages and prices warranted more “forceful” restrictive actions from the BoE. For the week, the German Dax and London FTSE sank 3.38% and 1.96% w/w respectively.

Finally, in the U.S., investors reacted to the latest monetary policy decision from the U.S. Federal Reserve. As expected, the apex bank raised rates by 50bps to 4.25%, sending interest rates to their highest level since 2007. The latest hike caps a year in which the central bank raised rates by 425bps, and the Fed chairman Jerome Powell has indicated that the bank will raise rates further in 2023. At time of publishing, the NASDAQ, Dow Jones, and S&P 500 were down 2.02%, 1.28%, and 1.46% respectively. Finally, in the U.S., investors reacted to the latest monetary policy decision from the U.S. Federal Reserve. As expected, the apex bank raised rates by 50bps to 4.25%, sending interest rates to their highest level since 2007. The latest hike caps a year in which the central bank raised rates by 425bps, and the Fed chairman Jerome Powell has indicated that the bank will raise rates further in 2023. At time of publishing, the NASDAQ, Dow Jones, and S&P 500 were down 2.02%, 1.28%, and 1.46% respectively.

Domestic Economy: In November, headline inflation rose by 38 basis points to 21.47% y/y. The increase was primarily driven by fuel scarcity and demand frontload ahead of the festive season. We expect inflation to slow in December due to high base effect and strong year-end harvest.

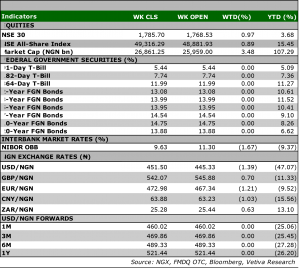

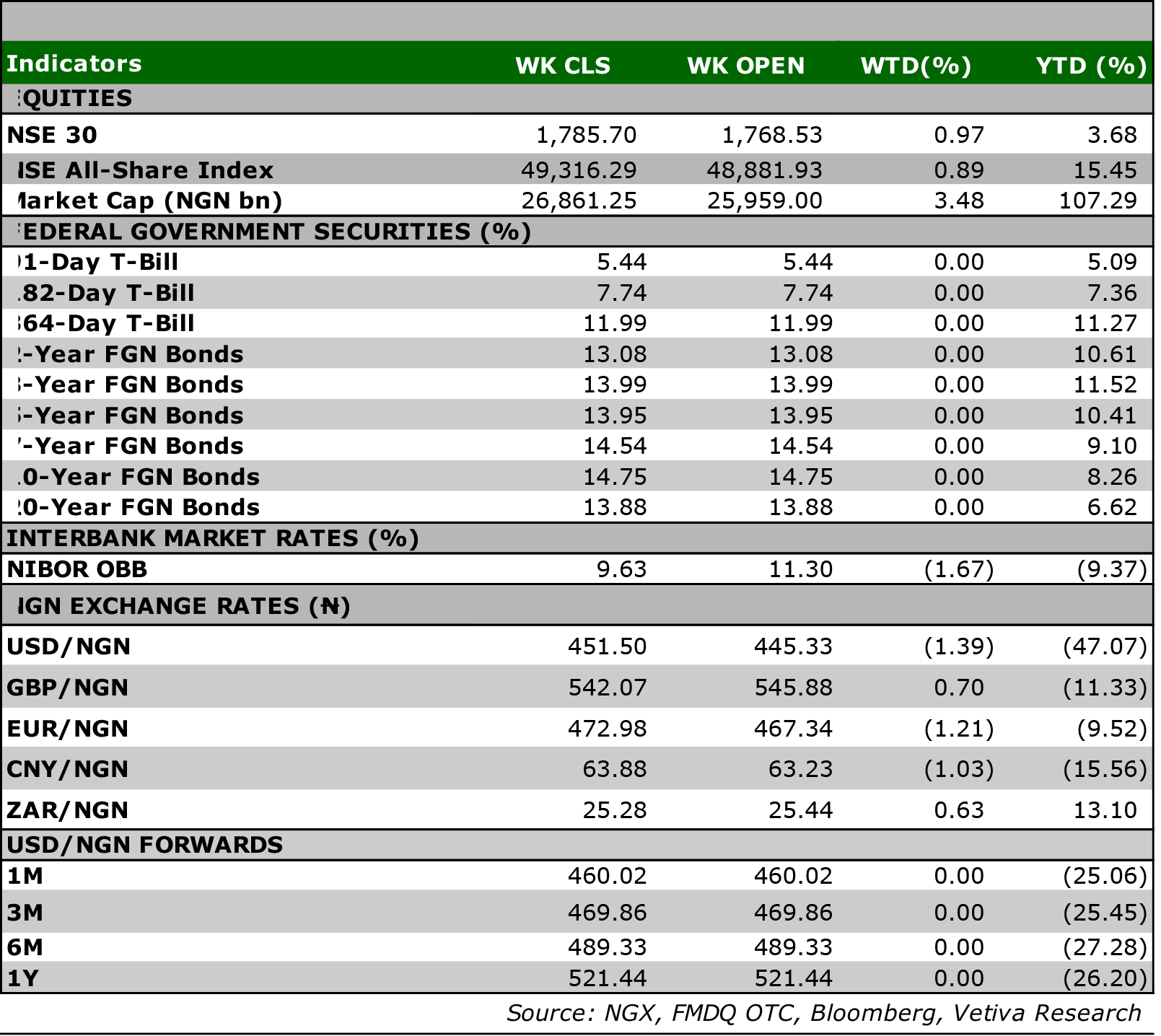

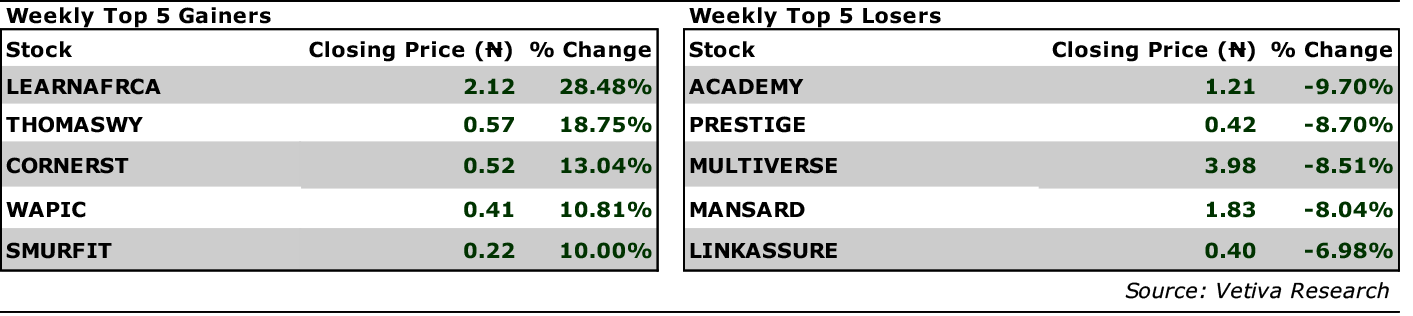

Equities: Investors were largely bullish across the equities market, as the NGXASI rose 89bps w/w to close at 49316.29pts. Banking stocks were the best performers for the week, as the sector gained 287bps w/w; of note, ZENITHBANK led the way, as the counter soared 905bps w/w; additionally, we saw interest in FIDELITYBK, which gained 241bps w/w. Likewise, in the Industrial Goods space BUACEMENT recorded another strong performance, rising 660bps w/w, fueling the 343bps w/w return for the Industrial Goods sector. Finally, interest the oil marketing space saw the Oil and Gas sector rise 0.36% w/w; ARDOVA was the top performing counter, rising 951bps w/w. On the other hand, investors turned bearish on the Consumer Goods space, as the sector lost 20bps w/w, dragged by profit-taking action in DANGSUGAR (-432bps w/w).

Fixed Income: On Monday, the Debt Management Office offered ₦225 billion and sold ₦264.51 billion across the 5-Year, 10-Year, and 15-Year tenors at stop rates of 14.60%, 14.75%, and 15.80% (Previous: 14.75%, 15.20%, 16.20%). As a result, of lower stop rates offered we saw aggressive buy-side action from investors over the course of the week, as the yield on benchmark bonds declined 63bps w/w on average. Meanwhile, it was a flat close across the NTB and OMO segments due to relatively tight system liquidity. Domestic Economy: In November, headline inflation rose by 38 basis points to 21.47% y/y. The increase was primarily driven by fuel scarcity and demand frontload ahead of the festive season. We expect inflation to slow in December due to high base effect and strong year-end harvest.

Equities: Investors were largely bullish across the equities market, as the NGXASI rose 89bps w/w to close at 49316.29pts. Banking stocks were the best performers for the week, as the sector gained 287bps w/w; of note, ZENITHBANK led the way, as the counter soared 905bps w/w; additionally, we saw interest in FIDELITYBK, which gained 241bps w/w. Likewise, in the Industrial Goods space BUACEMENT recorded another strong performance, rising 660bps w/w, fueling the 343bps w/w return for the Industrial Goods sector. Finally, interest the oil marketing space saw the Oil and Gas sector rise 0.36% w/w; ARDOVA was the top performing counter, rising 951bps w/w. On the other hand, investors turned bearish on the Consumer Goods space, as the sector lost 20bps w/w, dragged by profit-taking action in DANGSUGAR (-432bps w/w).

Fixed Income: On Monday, the Debt Management Office offered ₦225 billion and sold ₦264.51 billion across the 5-Year, 10-Year, and 15-Year tenors at stop rates of 14.60%, 14.75%, and 15.80% (Previous: 14.75%, 15.20%, 16.20%). As a result, of lower stop rates offered we saw aggressive buy-side action from investors over the course of the week, as the yield on benchmark bonds declined 63bps w/w on average. Meanwhile, it was a flat close across the NTB and OMO segments due to relatively tight system liquidity.

|

Moving to the European region, the latest rate hike from the European Central Bank dragged investor confidence, as they remain concerned about the impact of a restrictive monetary environment on the economy. The ECB raised its cash rate by 50bps to 2.00%, with ECB President Christine Lagarde telling market participants not to expect an early end to the current tightening stance of the ECB. The Bank of England also raised its cash rate as well by 50bps, with BoE governor Andrew Bailey stating that a constrained labor market, rising wages and prices warranted more “forceful” restrictive actions from the BoE. For the week, the German Dax and London FTSE sank 3.38% and 1.96% w/w respectively.

Moving to the European region, the latest rate hike from the European Central Bank dragged investor confidence, as they remain concerned about the impact of a restrictive monetary environment on the economy. The ECB raised its cash rate by 50bps to 2.00%, with ECB President Christine Lagarde telling market participants not to expect an early end to the current tightening stance of the ECB. The Bank of England also raised its cash rate as well by 50bps, with BoE governor Andrew Bailey stating that a constrained labor market, rising wages and prices warranted more “forceful” restrictive actions from the BoE. For the week, the German Dax and London FTSE sank 3.38% and 1.96% w/w respectively.

Finally, in the U.S., investors reacted to the latest monetary policy decision from the U.S. Federal Reserve. As expected, the apex bank raised rates by 50bps to 4.25%, sending interest rates to their highest level since 2007. The latest hike caps a year in which the central bank raised rates by 425bps, and the Fed chairman Jerome Powell has indicated that the bank will raise rates further in 2023. At time of publishing, the NASDAQ, Dow Jones, and S&P 500 were down 2.02%, 1.28%, and 1.46% respectively.

Finally, in the U.S., investors reacted to the latest monetary policy decision from the U.S. Federal Reserve. As expected, the apex bank raised rates by 50bps to 4.25%, sending interest rates to their highest level since 2007. The latest hike caps a year in which the central bank raised rates by 425bps, and the Fed chairman Jerome Powell has indicated that the bank will raise rates further in 2023. At time of publishing, the NASDAQ, Dow Jones, and S&P 500 were down 2.02%, 1.28%, and 1.46% respectively.

Domestic Economy: In November, headline inflation rose by 38 basis points to 21.47% y/y. The increase was primarily driven by fuel scarcity and demand frontload ahead of the festive season. We expect inflation to slow in December due to high base effect and strong year-end harvest.

Equities: Investors were largely bullish across the equities market, as the NGXASI rose 89bps w/w to close at 49316.29pts. Banking stocks were the best performers for the week, as the sector gained 287bps w/w; of note, ZENITHBANK led the way, as the counter soared 905bps w/w; additionally, we saw interest in FIDELITYBK, which gained 241bps w/w. Likewise, in the Industrial Goods space BUACEMENT recorded another strong performance, rising 660bps w/w, fueling the 343bps w/w return for the Industrial Goods sector. Finally, interest the oil marketing space saw the Oil and Gas sector rise 0.36% w/w; ARDOVA was the top performing counter, rising 951bps w/w. On the other hand, investors turned bearish on the Consumer Goods space, as the sector lost 20bps w/w, dragged by profit-taking action in DANGSUGAR (-432bps w/w).

Fixed Income: On Monday, the Debt Management Office offered ₦225 billion and sold ₦264.51 billion across the 5-Year, 10-Year, and 15-Year tenors at stop rates of 14.60%, 14.75%, and 15.80% (Previous: 14.75%, 15.20%, 16.20%). As a result, of lower stop rates offered we saw aggressive buy-side action from investors over the course of the week, as the yield on benchmark bonds declined 63bps w/w on average. Meanwhile, it was a flat close across the NTB and OMO segments due to relatively tight system liquidity.

Domestic Economy: In November, headline inflation rose by 38 basis points to 21.47% y/y. The increase was primarily driven by fuel scarcity and demand frontload ahead of the festive season. We expect inflation to slow in December due to high base effect and strong year-end harvest.

Equities: Investors were largely bullish across the equities market, as the NGXASI rose 89bps w/w to close at 49316.29pts. Banking stocks were the best performers for the week, as the sector gained 287bps w/w; of note, ZENITHBANK led the way, as the counter soared 905bps w/w; additionally, we saw interest in FIDELITYBK, which gained 241bps w/w. Likewise, in the Industrial Goods space BUACEMENT recorded another strong performance, rising 660bps w/w, fueling the 343bps w/w return for the Industrial Goods sector. Finally, interest the oil marketing space saw the Oil and Gas sector rise 0.36% w/w; ARDOVA was the top performing counter, rising 951bps w/w. On the other hand, investors turned bearish on the Consumer Goods space, as the sector lost 20bps w/w, dragged by profit-taking action in DANGSUGAR (-432bps w/w).

Fixed Income: On Monday, the Debt Management Office offered ₦225 billion and sold ₦264.51 billion across the 5-Year, 10-Year, and 15-Year tenors at stop rates of 14.60%, 14.75%, and 15.80% (Previous: 14.75%, 15.20%, 16.20%). As a result, of lower stop rates offered we saw aggressive buy-side action from investors over the course of the week, as the yield on benchmark bonds declined 63bps w/w on average. Meanwhile, it was a flat close across the NTB and OMO segments due to relatively tight system liquidity.